Short Term Volatility > Long Term Clarity

Everyone is fully aware that over the weekend, Israel and the U.S. launched military strikes against Iran, killing senior leadership including Ayatollah Ali Khamenei. Market reactions were muted on Monday except for a spike in oil prices. With the fears of a more prolonged and spreading conflict, volatility is following suit. Concerns of increased inflation - wars are overwhelmingly inflationary due to increased government spending, resource scarcity and supply chain disruptions - add fuel to the fire.

As we write this, the major indexes - the S&P 500, Dow Jones Industrial Average, and Nasdaq Composite - have all been choppy. International equity markets are reacting more negatively, as those economies are more reliant on oil from the Middle East. Oil (Brent crude) spiked 20% over the past month, with most of the increase in the last several days. The VIX volatility index moved back above 20. Energy and defensive sectors, like consumer staples and utilities, have led early in 2026, while some of last year’s high-flying tech names have cooled off.

It feels like a lot. Because it is.

We’re dealing with trade and tariff uncertainty, Ongoing AI valuation questions, Middle East tensions, Sticky inflation conversations. It’s not just one thing…it’s everything happening at once and that’s the backdrop where “boring” works.

A Little Perspective

There’s an old line from Warren Buffett that’s worth revisiting:

“We simply attempt to be fearful when others are greedy and to be greedy only when others are fearful.”

Moments like this test that discipline.

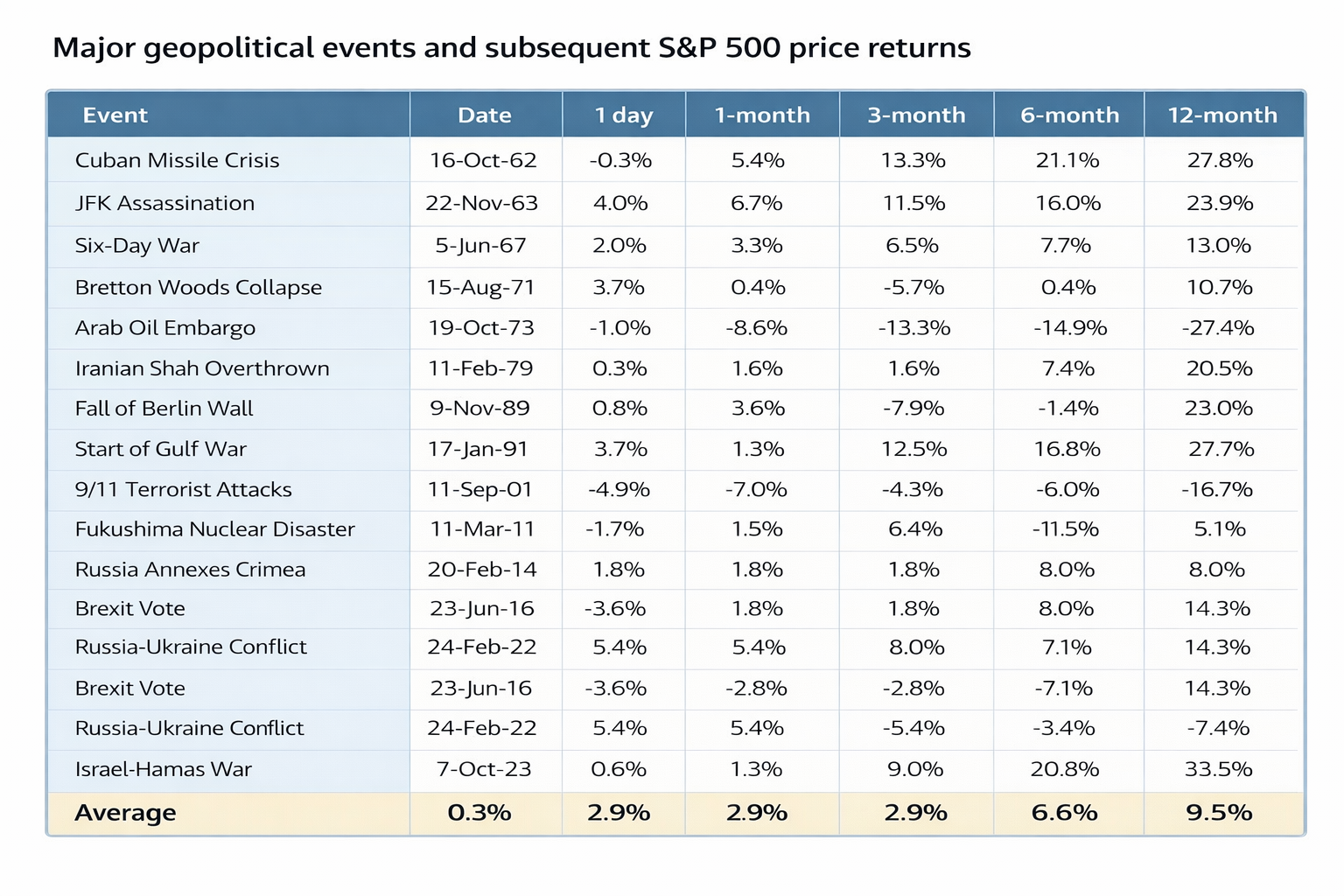

Historically, geopolitical shocks create near-term volatility, sometimes sharp volatility. But when the underlying economy is stable, markets have typically recovered in the months that follow. In most past crises, the median return for the S&P 500 six to twelve months later has been positive. That doesn’t mean markets can’t fall further in the short run, they absolutely can. It reminds us that reacting emotionally to headlines has rarely been a winning long-term strategy.

What Actually Matters for Markets

The real primary driver here isn’t the headlines, it’s energy and uncertainty. If oil were to surge and stay well above $100 for a sustained period, that could meaningfully pressure inflation and interest rates. That’s something we’re watching closely.

It’s also important to remember:

- The U.S. is now a net energy exporter, very different from the 1970s.

- Domestic production can ramp faster than it once could.

- Much of this conflict had been partially priced in as tensions built over the past month.

Meanwhile, the broader U.S. economic backdrop remains reasonably solid. The labor market continues to hold up, corporate earnings have been resilient, fiscal policy still provides some tailwind and growth is steady.

Our Positioning: Stay Invested, Reduce Volatility, Get Paid to Wait

In this type of geopolitical climate, this is not the time to play offense.

Matt said this verbatim on CNBC last week…our approach is simple: stay invested, reduce volatility, lean defensive where appropriate, and get paid to wait. Link below:

We’ve already seen rotation this year toward energy, staples, and other more defensive areas. When uncertainty rises, capital tends to move toward cash flow, dividends, and real assets.

Our base case for 2026: mid-single to low double digit equity returns remains intact. The conflict does not fundamentally alter our long-term outlook. We expect increased volatility until more clarity is seen with the Iran conflicts.

The Bigger Picture

There are always geopolitical risks…always. From wars to assassinations to financial crises, markets have faced decades of elevated tension and yet over time, they’ve continued to grind higher. Often the bigger damage comes not from the geopolitical event itself, but from an underlying economic downturn that was already forming.

Scoping out, it’s possible that near-term instability leads to longer-term regional stabilization. That would come with short-term market costs, but potentially longer-term benefits. We’ll continue to assess that as events unfold.

Final Thought

We know volatility is uncomfortable. It’s supposed to be, it’s the price of admission for long-term returns. Our job isn’t to predict every headline. It’s to build portfolios that can navigate uncertainty…whether it’s geopolitical tension, AI disruption, inflation debates, or all of the above at once.

We won’t always get every call perfectly right, but we will stay disciplined, will stay diversified, and will stay focused on long-term outcomes.

As always, if you have questions, reach out. That’s what we’re here for.

Source: Bloomberg. Data as of January 26, 2026. If the market was closed on the event date, the date of the previous market close was referenced. The one-day return for the 9/11 attacks

after reopening of the market was on 9/17/2001. The one-day return for the JFK assassination after the reopening of the market was on 11/26/1963. FOR INFORMATIONAL PURPOSES ONLY.

Indexes are unmanaged and do not take into account fees or expenses. Past performance is no guarantee of future results. Please refer to important disclosures at the end of this report.